GST Compliance Explained: Common Errors Businesses Make and How to Avoid Them

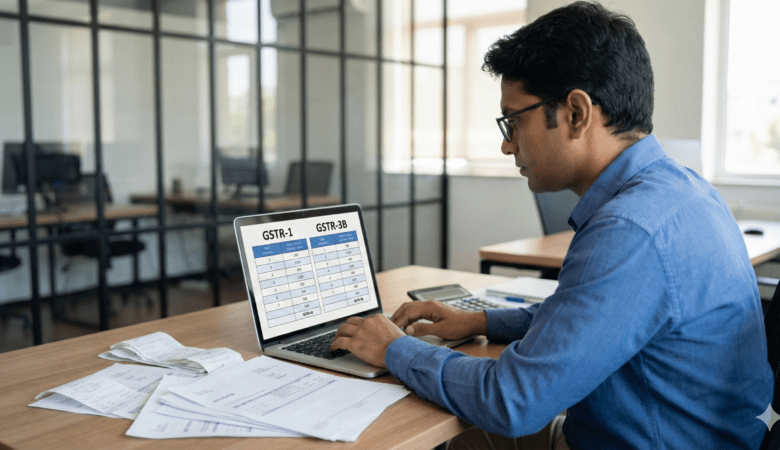

Goods and Services Tax (GST) is one of the most significant reforms in Indian taxation, designed to simplify indirect taxes and create a uniform tax system. However, many businesses, especially small and medium enterprises, face challenges in staying compliant. Mistakes in GST compliance can lead to penalties, delayed refunds, and unnecessary legal scrutiny. In this blog, we’ll discuss common GST errors businesses make and provide tips to avoid them effectively. 1. Late Filing of GST Returns Common Mistake: Filing returns after the due date. Why it happens: Businesses may forget deadlines or struggle with inadequate bookkeeping. Impact: Interest and penalties under Section 47 of the CGST Act. Delayed input tax credit (ITC) claims. How to avoid: Maintain a monthly calendar for GST filings. Use accounting software with automated GST reminders. Plan submissions well in advance to avoid last-minute rush. 2. Incorrect or Incomplete Invoicing Common Mistake: Errors in GST invoices, such as: Wrong GSTIN of supplier or recipient. Incorrect tax rates. Missing invoice numbers or dates. Impact: Rejection of input tax credit by the recipient. Penalties for non-compliance. How to avoid: Use standardized invoice templates. Double-check GSTINs, HSN/SAC codes, and tax rates. Maintain proper invoice numbering and documentation. 3. Mismatch Between GSTR-1 and GSTR-3B Common Mistake: The data in GSTR-1 (outward supplies) does not match GSTR-3B (summary return). Impact: ITC claims can be denied. Notices from the GST department. How to avoid: Reconcile invoices regularly before filing. Automate reconciliation with accounting software if possible. Keep supplier invoices verified and updated. 4. Wrong Claim of Input Tax Credit (ITC) Common Mistake: Claiming ITC on non-eligible goods or services, or on invoices without proper GST compliance. Impact: ITC reversal, interest, and penalties. Increased scrutiny from GST authorities. How to avoid: Check eligibility under Section 16 of the CGST Act. Maintain proper supporting documents. Reconcile ITC monthly with supplier data. 5. Ignoring E-Way Bill Requirements Common Mistake: Transporting goods without generating e-way bills where required. Impact: Penalties and fines during transit. Delays in delivery due to inspections. How to avoid: Understand e-way bill applicability based on distance, value, and type of goods. Generate e-way bills in advance using online portals or integrated software. 6. Non-Maintenance of Proper Records Common Mistake: Incomplete or disorganized GST records. Impact: Difficulty during audits. Increased risk of penalties for incorrect filings. How to avoid: Maintain all invoices, bills, and payment records systematically. Implement accounting software to store digital records securely. Conduct periodic audits to ensure compliance. 7. Incorrect Classification of Goods and Services Common Mistake: Applying wrong HSN (Harmonized System of Nomenclature) or SAC (Service Accounting Code) codes. Impact: Wrong tax rates applied. Notices from GST authorities and potential penalties. How to avoid: Refer to official HSN/SAC lists provided by GST authorities. Seek professional help if unsure about classifications. Conclusion GST compliance is critical to maintain smooth business operations and avoid unnecessary penalties. By staying organized, using technology, and seeking professional guidance when needed, businesses can significantly reduce the risk of errors. Remember, even small mistakes can lead to denied ITC, penalties, and legal complications. Ensuring accurate GST compliance is not just a statutory requirement—it’s a smart business practice that protects your revenue and credibility.